Almost all listed companies now regularly conduct a so-called ESG materiality analysis. We explain why there is more to it than just a costly market research operation – and show what a pragmatic and cost-efficient materiality analysis looks like.

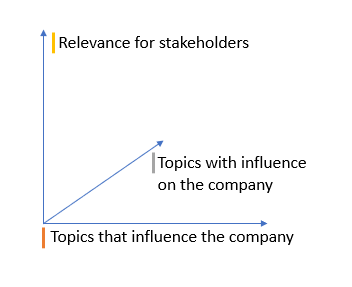

An ESG materiality analysis forms the basis for the development of a company’s sustainability strategy. For this purpose, the most important internal and external stakeholders are asked about their assessment of which ESG topics are particularly important for the company in question – and which aren’t. Three dimensions should be captured and assessed in an ideal ESG materiality analysis:

- Key ESG topics for stakeholders [according to GRI].

- Key ESG topics influencing the company [according to GRI and CSRD].

- Key ESG topics that the company influences [according to CSRD].

A Materiality Analysis in 4 Steps

A fixed procedure for conducting an ESG materiality analysis has not yet been established. But a four-step process can be derived from the best practices of other companies and various frameworks such as the Global Reporting Initiative (GRI) and the Standard AA1000.

1. Identification of Relevant Stakeholders

In order to be able to contact stakeholders, they must first be identified. Internal stakeholders are often quickly determined: depending on the corporate structure, these are internal groups such as employees, the management board or the supervisory board.

For the external view, it is often necessary to think more broadly, because in principle this includes not only customers or investors, but also suppliers, NGOs, the media or political actors. The relevance of each of these stakeholder groups should be determined internally in advance, because not every group is equally important for the company and equally affected by its decisions. This determination should be made by people in the company, who ideally work in different areas, in order to obtain as realistic a picture as possible of the most important external stakeholders.

Best practice: In its current sustainability report, ZEAL transparently presents how the most important stakeholders were determined. It has based this on the AccountAbility-Standard AA1000. This standard recommends evaluating stakeholders according to the dimensions “dependency,” “responsibility,” “tensions,” “influence,” and “different perspectives“.

2. Topic Determination for the Survey

In a second step, the relevant ESG topics for the interviews during the ESG materiality analysis are identified. In addition to industry-specific statutory ESG requirements and those of established frameworks such as SASB or WEF, the topics of the materiality analyses of companies from the same industry are a pragmatic starting point. The procedure may seem simple – but the trick is to define relevant topics without overlaps.

Best practice: In its sustainability report, the GLS Bank lists the top 20 topics that were considered relevant during its own ESG materiality analysis. In the overview, the topics are classified according to relevance and divided into the four fields “Core business”, “Operational objectives: Ecology,” “Operational goals: Social” and “Political and social commitment”.

3. Asking the Stakeholders

Once the topics have been identified, they can now be passed on to the defined stakeholders to evaluate their respective relevance. The most common methods are (quantitative) surveys or (qualitative) interviews with the relevant stakeholders. If you would like to gain even more insights as part of the analysis, you can hold workshops to jointly identify key topics. In particular, surveying stakeholders outside the company makes it possible to gain a holistic and realistic view of the company’s activities and its influence on ecological and social issues. Important questions during the assessment include: How important is this topic for our external partners and stakeholders? How is the topic evaluated within the company? What influence does it have on the company’s goals?

During the survey, however, a fundamental problem can arise: stakeholders do not respond or the responses are not sufficient to sustain a robust data basis. In such cases, incentives – and of course (friendly) reminders – can help. After all, a differentiated picture for the topic evaluation can only be achieved through an appropriate number of feedbacks from different stakeholders.

4. Evaluation of the Topic Assessment – Materiality Matrix

In the final step, the topics weighted according to the survey are entered into a “materiality matrix” (see figure below). In this matrix, the weighting of topics by stakeholders and companies can be read. The y-axis indicates the relevance of the stakeholders’ topics, while the x- and z-axis show the prioritization by the company. The upper right quadrant shows the prioritization of the topics that have been classified as important by both the company and the stakeholders. Ideally, this matrix should also be included in the sustainability report so that readers can get a clear picture of the relevant topics. It is important to note that conflicting assessments are permitted and should be disclosed. Dealing with conflicting goals is in turn a good starting point for the subsequent defintion of a sustainability strategy. It plays a key role in ensuring that the company’s own actions are repeatedly compared with internal and external expectations.

Best practice: Rügenwalder Mühle‘s materiality matrix clearly shows the most important topics for the company. The color coding makes it easy to categorize the terms into the four areas of “sustainable corporate management,” “environment,” “economy” and “social affairs”. In the accompanying text, the most important topics for the company are again emphasized.

Strategic Consequences

Finally, the topics that have been identified as particularly important should form the basis for the company’s sustainability strategy. The ESG materiality analysis makes it possible to identify individual focus points in the environmental, social and governance areas, from which concrete strategic measures for the company and initial ESG targets can then be derived, which helps companies to take their ESG agenda into their own hands.

You would like to conduct a materiality analysis in your company that does not overburden your organization? We will find the right solution with you – don’t hesitate to get in touch!