But where to start with ESG reporting? The CSRD requires a materiality analysis to be carried out. Two dimensions are considered: the most important influences of the company on environmental and social issues (impact perspective) – and material risks and opportunities arising for the company from environmental and social issues (risk-and-opportunity perspective). These two perspectives of materiality analysis are also referred to as the principle of “double materiality”.

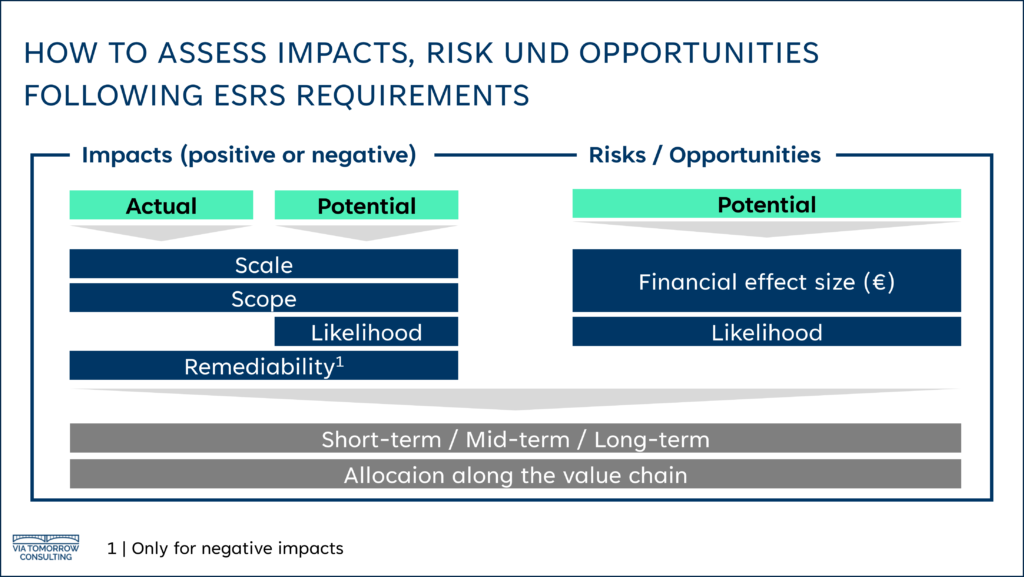

For internal and external stakeholder engagement, companies must consider all topics provided for in the ESRS (European Sustainability Reporting Standards) of the CSRD, as well as other company-specific topics. With the help of internal and external stakeholders, Impacts, Risks and Opportunities (IROs) must be assessed for each topic. The impacts are assessed using the evaluation categories “Scope,” “Scale,” “Remediability,” “Time Horizon” and – if potential impacts are involved – “Likelihood. Risks and oppportunties are assessed using the categories “Likelihood,” “Financial Effect Size,” and “Time Horizon.

In view of the complexity of the underlying ESG issues, expert assessments play a key role in these assessments. For this purpose, the ESRS provide for the consultation of both internal and external contacts (stakeholders). The latter are to be centrally involved in the inside-out perspective, as they are or could be directly or indirectly affected by possible impacts.

The assessment of all IROs provides information on which issues are material for the company. These form the cornerstone for further ESRS reporting: based on the materiality analysis, companies may delete immaterial ESG topics for their reporting, but must be all the more transparent with all material topics. This includes defining goals and action plans, creating relevant guidelines, and disclosing detailed metrics.